![]()

RASAMEEL GCC UPDATE June 2015

Article Overview

Over the last month banks in the UAE have preferred conventional bond issuance whilst Saudi corporates have taken the Sukuk route.

UAE Banks Issue Conventional Bonds

Bank of Sharjah and National Bank of Abu Dhabi both issued conventional bonds over the course of the last month, whilst Etihad Airways is in talks with investors for a potential bond issue.

Bank of Sharjah priced a five year dollar denominated bond worth USD 500 mn at the coupon rate of 3.37%. The deal attracted huge investor demand, resulting in an oversubscription of more than 2.0x. JP Morgan and National Bank of Abu Dhabi were the joint coordinators, and others including Commerzbank, Emirates NBD Capital and First Gulf Bank were the book runners to the deal.

National Bank of Abu Dhabi (NBAD), UAE’s largest bank by assets, issued a USD 750mn non-call able five-year perpetual Tier1 bond at 5.25%. The bond is rated six notches lower than the lender’s rating at Baa3/BBB-by both Moody’s and S&P respectively. Citigroup, HSBC, Morgan Stanley, Societe Generale and NBAD’s own investment banking were the arrangers for the deal.

Etihad Airways ,the Abu Dhabi Government owned airline, is in talks with potential investors for a USD1bn bond issuance. The proceeds from the issue would be lent to its global partners to fund expansion plans. The bond will not be guaranteed by Etihad, hence is likely to berated junk. The company is in talks with Goldman Sachs and National Bank of Abu Dhabi to enlist them as lead arrangers for the transaction.

Sukuk Activity in Saudi Arabia

Riyad Bank, Saudi Arabia’s fourth largest lender by asset, issued a 10-year capital boosting sukuk worth SAR4bn (USD1.07bn) at a profit rate of 115bps+ 6M SIBOR. The privately placed sukuk remains callable after five years.

Saudi Arabia’s National Commercial Bank (NCB) raised SAR 1bn through a capital boosting sukuk in order to enhance its Tier1 capital. The privately placed sukuk was Base lIII compliant with a perpetual tenor, however can be called back at a predefined date.

Also within the Kingdom Najran Cement has raised SAR400mn (USD106.7mn) through an Islamic bond issuance of five-years maturity. The sukuk was privately placed and has been priced at 1.4% +3M SIBOR.

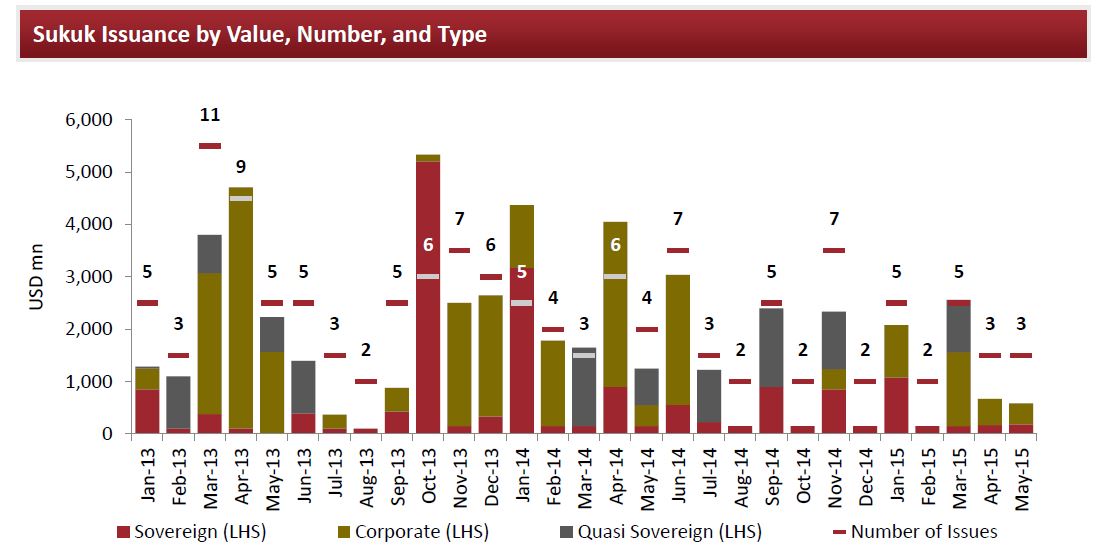

GCC Sukuk Issuance up to June 2015 – Year on Year

Download

Download Rasameel GCC Market Update June 2015 ![]() (800KB)

(800KB)