Insurance enables households and corporations to live and operate in a stable environment. It facilitates economic transactions by providing risk transfer and indemnification. It also promotes financial stability, enables risks to be managed more efficiently and fosters efficient capital allocation. The Islamic (takaful) insurance industry is an important segment of the Islamic financial system. It complements the other segments and acts as a risk-sharing channel to help withstand financial shocks. A robust Islamic insurance industry helps to leverage risks at IIFSs, creates market synergies and provides the base for accelerating the next phase of industry growth.

The Islamic insurance industry has developed remarkably over the last four years. Indeed, the number of Islamic insurance companies grew by nearly 73% between 2008 and 2010 (i.e. from 113 to 195), with these being based in more than 30 countries. Their number is expected to increase further in the near future, as the industry’s growth gathers momentum. It should be noted that in the five years from 2006 to 2011, the Islamic insurance industry enjoyed a compound annual growth rate of 20%, which was significantly higher than the growth of approximately 6-8% displayed by its conventional counterpart.

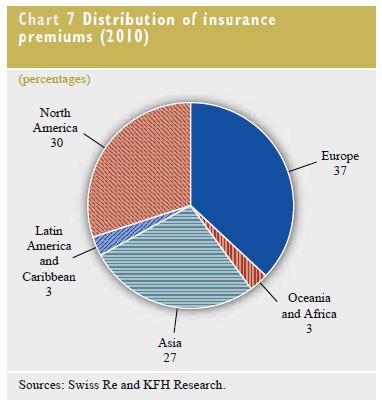

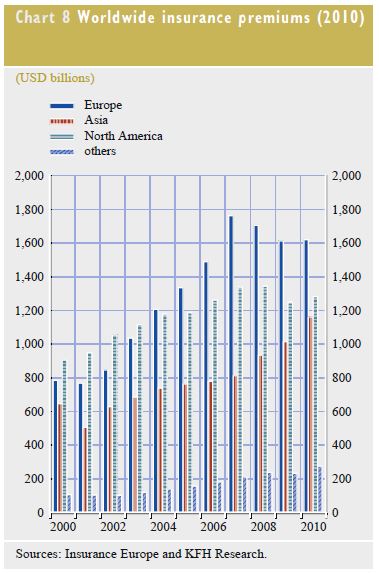

Insurers are among the largest institutional investors in Europe. European insurers generate a premium income of almost €1.1 trillion (and thus account for more than one-third of the global insurance market; see Charts 7 and 8), employ nearly one million people and invest

around €7.7 trillion in the economy. Given its depth, the European insurance industry is an established and fully-equipped vehicle for the

introduction of Islamic insurance operations.

Furthermore, the European market is familiar with the concept of “mutuality and cooperative insurance”. which has many similarities with

Islamic insurance. In fact, more than two-thirds of all insurers in Europe belong to the mutual and cooperative insurance sector. Mutual and

Islamic insurance share the principle of risksharing, with risks being spread over members/ participants. All of these are key factors that

should help Islamic insurance make headway in the European market.

The growth of Islamic finance in Europe has largely been concentrated in the Islamic banking and Islamic capital market segments. But as these segments grow, Islamic insurance could become a key complementary offering for consumers who are seeking Islamic financial solutions. Islamic mortgage insurance, for example, would fit some Islamic financial instruments, particularly Islamic retail banking products and services.

The regulatory reforms across Europe have helped to accelerate the expansion of Islamic insurance products and services in this region. The

mandatory “European Single Passport” instituted in December 2002 allows insurance providers registered in an EU Member State to offer their

services to the whole European market, and thus promotes the penetration of new markets.

This will speed up the introduction of Islamic insurance across Europe. However, the possible adoption of the Solvency II Directive essentially a capital adequacy regime for insurance firms) by the European Parliament and the Council of the European Union could also challenge the ability of Islamic insurers to meet solvency and risk management guidelines. The regulation’s concern about “concentration risks” may require Islamic insurance providers to have a portfolio that is sufficiently diversified across and within different asset classes. This would be difficult to achieve, given the scarcity of Shari’ah-compliant solutions in specific jurisdictions. Nonetheless, this scarcity should subside as Islamic finance gains momentum in Europe.

BALJEET KAUR GREWAL

European Central Bank